Orlando, Fla. — The scope of workers compensation coverage has broadened considerably since its early beginnings. In 1972, states amended their laws to meet performance standards recommended by the National Commission on State Workmen's Compensation Laws. Many states took action not only to expand benefits but also to make the coverage applicable to classifications of employees not previously covered.

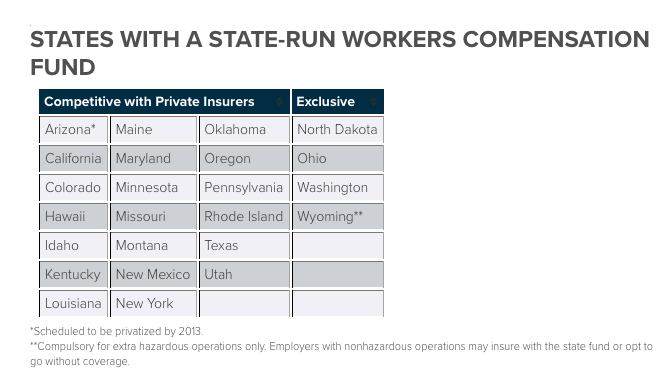

Workers compensation systems are administered by the individual states, generally by commissions or boards whose responsibility it is to ensure compliance with the laws, investigate and decide disputed cases, and collect data. In most states employers are required to keep records of accidents. Accidents must be reported to the workers compensation board and to the company’s insurer within a specified number of days. The only state in which workers compensation coverage is truly optional is Texas, where about one-third of the state’s employers are so-called non subscribers. In the event of a serious accident, those that opt out of the system can be sued by employees for failure to provide a safe workplace.

As you can see, workers compensation systems vary from state to state. State statutes and court decisions control many aspects, including the handling of claims, the evaluation of impairment and settlement of disputes, the amount of benefits injured workers receive and the strategies used to control costs. According to the U.S. Chamber of Commerce, from 2013 to 2014 maximum income benefits for total disability increased an average of 1.87 percent.

The National Council on Compensation Insurance will be hosting their Annual Issues Symposium this year at the Hyatt Regency Grand Cypress Resort in Orlando on May 16-18, 23018. We look forward to get more active in our State’s decisions involving this important subject for employers of all sizes while dealing with the challenges that are foreseen to come in the near future.

The most recent developments have been:

National: According to NCCI’s State of the Line analysis, in 2013 workers compensation premiums for private carriers and state funds increased to $41.9 billion, the highest level since 2007. Premiums for private carriers alone grew to $37 billion from $35.1billion, a jump of 5.4 percent from 2012 as employment figures moved up toward pre-financial crisis levels. Because its premiums are directly linked to employment and wages, workers compensation insurance was the line most significantly affected by the economic slowdown.

Premiums for the residual market grew from $0.8 billion to $1.1 billion, and its market share rose from 7 percent to 8 percent as the market tightened. The increase was driven primarily by larger companies.

The combined ratio, the percentage of each premium dollar spent on claims and expenses, was 101 for private insurers, the lowest since 2009 and a significant improvement over the 108 figure for 2012. The combined ratio for the 16 state funds administered by the NCCI was 115, compared with 124 for the previous year. A combined ratio of 100 or higher means that the industry is paying out more in claims than it is collecting in premiums.

Lost-time claim frequency (the number of claims that include loss of income due to time off work as opposed to solely medical care claims) dropped 2 percent, continuing a trend that has been going on for many years. (Overall, claim frequency dropped 58.3 percent from 1991 to 2012.) The cost of claims increased slightly.

Obesity has an impact on the cost of claims, according to a study by the National Council on Compensation Insurance. The study revealed that the duration of lost income claims was five times greater for the most severely obese workers than for workers who were not obese but filed comparable claims. This data came from insurers operating in 40 states and the study’s findings are similar to those of a 2007 Duke University Medical School report on its own employees.

In Garzor Insurance, we are committed to provide knowledge and the best customer service. Being on top of the insurance issues that affect the State of Florida is our priority in order to offer you real coverage solutions for your business.